In order for AI to be sustainable, two races have emerged: the race for efficient energy and the race for efficient computing. The race for energy has a head start with existing solutions such as renewables and nuclear. The computing race is a little different, much younger, and certainly making headlines. Introducing: quantum computing.

A leader emerging in this young industry is IonQ, Inc. (IONQ), a company that is researching and developing a scalable quantum computer. As with any innovative and speculative market, whoever creates the damn thing gets the glory, this much is obvious. What I hope to accomplish in my analysis is to show you the gravity of that glory and whether or not IONQ can carry that glory.

This analysis will be a bottom-up approach, starting with alarming fundamentals and moving to international obstacles.

I. Alarming Fundamentals

A typical macroeconomics to company analysis begins at the broader level, starting with signals of demand at a global level and moving down to the company’s ability to capitalize on those signals. Quantum computing being such a young industry, there is difficulty finding quantitative signals for such a market.

Interestingly enough, IONQ’s fundamentals encompass the world’s perspective on quantum computing quite well.

- Since 2021, IONQ’s annual revenue increased by approximately 2050%, growing from $2M in 2021 to $43M in 2024.

- Since 2021, IONQ’s annual research and development cost has also increased by 1248%, growing from $10M in 2020 to $137M in 2024.

- Cashflow from financing activities increased from $39M in Q4’24 to $369M in Q1’25.

While these numbers are specific to IONQ, I believe this paints a picture for quantum computing at a high level: aggressive and increasing demand, even more aggressive research and development by firms within the industry, and investors seeing value and need for quantum computing.

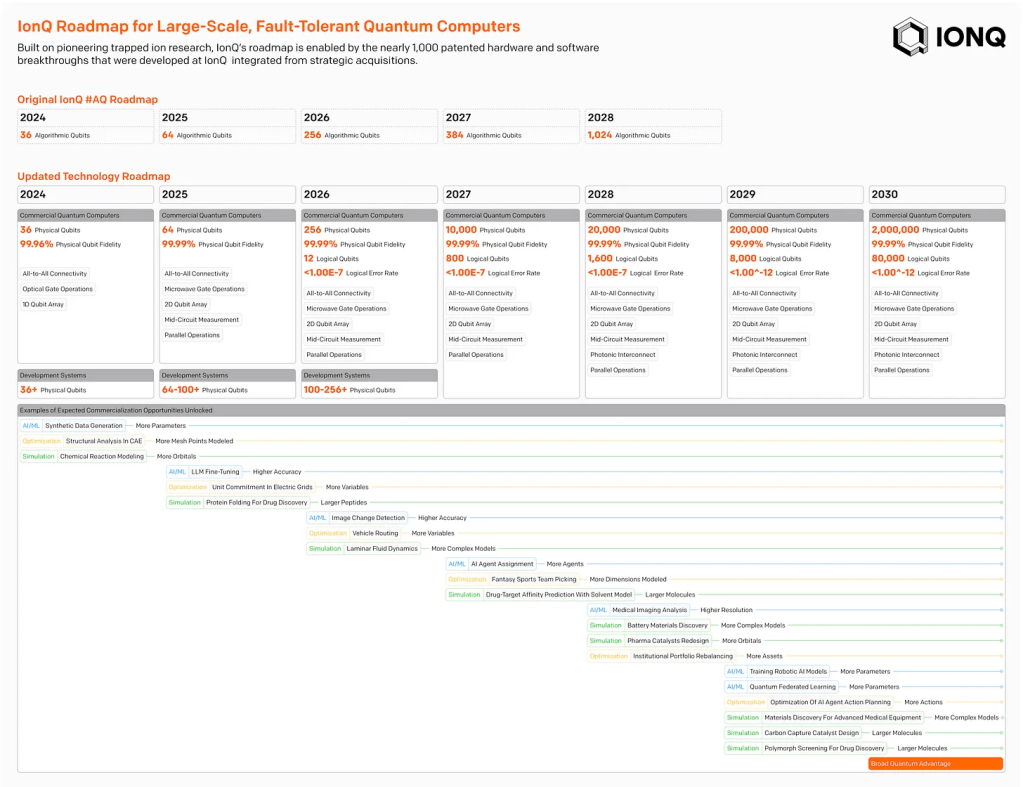

Another aspect of IONQ I want to bring to attention is their accelerated roadmap. IONQ has not made any public disclosures of missed milestones or timeline extensions. However, what is far more representative of the larger picture is the literal timeline itself. Currently, the plan scales into 2030, which aligns with experts stating that practical use of quantum still ranges from 5-15 years.

Simply from IONQ’s profile, we have a picture of the industry: aggressive demand, even more aggressive R&D, investors seeing high potential value, and a timeline that warns investors of the distance ahead of them.

II. Labor Market and Quantum Life Cycle

Quantum is estimated to create 840,000 new jobs by 2035 and 250,000 by 2030. However, there have been current shifts in the market for quantum showcasing itself, with LinkedIn statistics stating “quantum” related roles have increased by 180% between 2020-2024. Additionally, quantum companies aren’t just limiting their workforce to PhDs and engineers but also high school degrees, as companies need technicians, developers, and analysts.

I wanted to draw attention to this movement as it is clear, to support R&D, companies and markets are taking an active approach to widening the bottleneck of the labor force by widening the criteria of qualifications.

However, I believe that because there is no clear title for the workforce, that goes to show just how young and undiscovered this industry is to the general public.

III. What VC and government funding tell us about AI

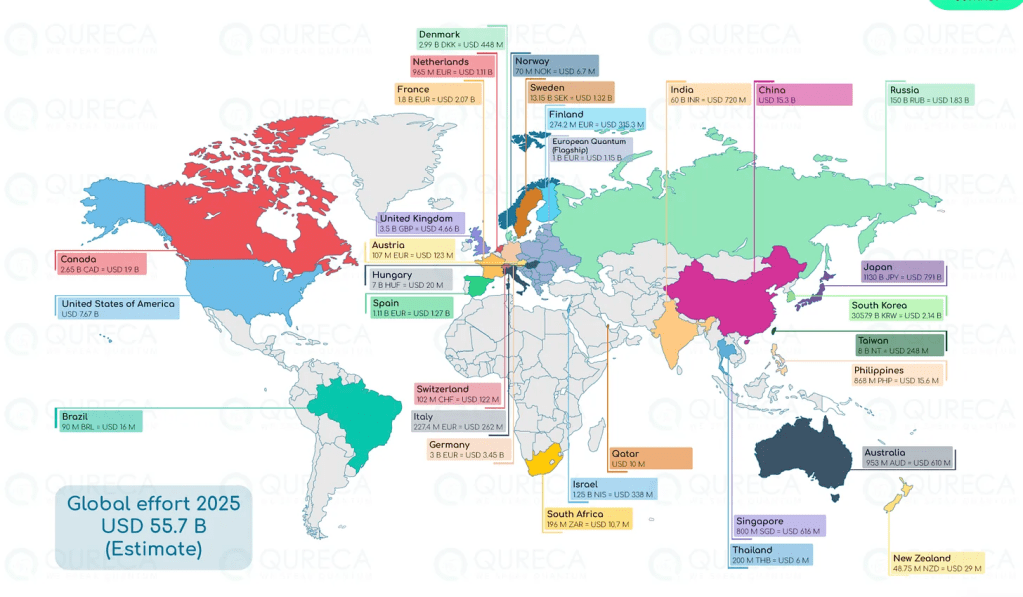

In 2024, quantum computing startups were estimated to raise $1.5B in venture funding. In 2025, the global investment is estimated to be $55.7B with investment in the US ($7.67B), Japan ($7.91B), and China ($15.3B), leading the charge.

Investments aren’t just coming from the private sector. Initiatives such as the National Quantum Initiative Act in 2018 by the US, the European Quantum Flagship, and China announcing a national venture guidance in March 2025. Large movements from both the public and private sectors are pushing development with an estimated global market of $106B by 2040.

Specific to IONQ, notable partnerships and investors include NVDIA, AWS, Hyundai, Toyota, and General Dynamics.

The large movements behind quantum can also tell another story: the growth of AI is unsustainable.

IV. China PMI + Rare earths mining + Tariffs (US + China Deal)

In order for quantum to function, it requires a very cold environment. This environment requires rare earth metals. China dominates this market, owning 70% of the globe’s rare earth mines and 90% of the globe’s rare earth processing facilities. This is subject to change, especially as quantum’s demand grows. But this grasp of key resources is the kind of mountain that can slow progress.

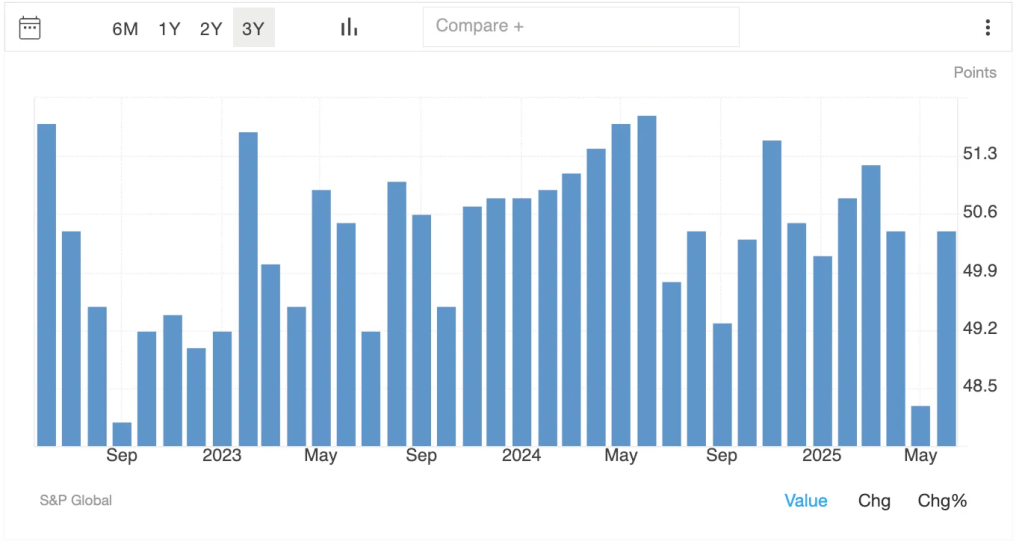

It is particularly difficult to measure China’s mining progress, but I decided to use their PMI as a close estimate. China PMI unexpectedly rose to 50.4 in June ’25, up from 48.3 in May ’25; however, it has been showing a downward trend since June ’24.

While the US and China have seemingly been able to strike a deal regarding rare earths, continuous tariff threats will put pressure on costs for quantum companies.

Summary and Analysis

Quantum computing seems to have gained the census that it is less of a question of ‘if’ and more of a question of ‘when. But that ‘when’ might not arrive in a timely fashion. IONQ shows a roadmap for 5 years, Jensen Huang has stated 20+ years, and I have seen other sources range from 10-15 years. From any angle, quantum seem less like ‘quick money’ and more like ‘heavy and far away money’.

Often, tech is seen as a highway to riches when in reality its a long hold, filled with crushing volatility. IONQ should not be any different.

In an obviously speculative market, IONQ is trying its very best to transparent. Public revenues, R&D costs, and roadmaps can be a double edged sword as it communicates to investors what’s working but spotlight what’s not.

Strong investor confidence makes it difficult to see what would kill this stock. However, any signs of a weak economy, roadmap delays, a new competitor, increased politcal/tariff tensions, or even lack of news will certainly depress this stock’s growth, more so than any other industry.

My Take

As boundaries for AI are pushed so do the scarcity of resources. The future of AI involves more complicated problems and that requires a more efficient energy intake and a more efficient computing system. The current growth of AI isn’t sustainable and corporations are aware of this.

Combine the search for sustainable AI growth with public communication/accomplishments, and IONQ has a bullish future. More than anything though, IONQ has a difficult task of maintaining investor confidence and attention in the long-term.

It’s clear that IONQ has not reached its full potential but road ahead is far from smooth. I believe investors looking to jump in should be prepared for a long haul and to not let the time in an investment become an attachment. I will be cautiously monitoring and looking to invest in the coming months.

Leave a comment