Paying attention solely to the US stock market, one would assume that 2026 kicked off like any other year. The capture of a Venezuelan President, threats of a Greenland takeover, the dollar sinking, and a deliberate attack on the Federal Reserve independence have yet to dent markets.

The recent history of abysmally low market reactions or violent returns to market highs has left experts baffled. Perhaps the mounting volatility has finally created a “resilient” stock market, one undeterred by mere invasions or the possible collapse of foundational economic institutions.

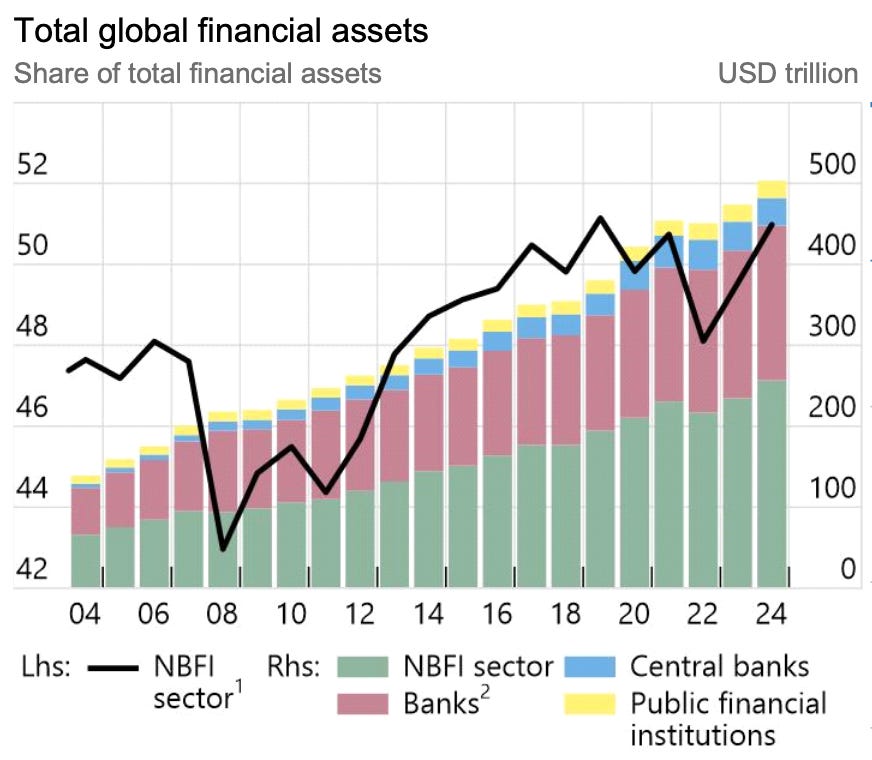

Underneath the surface, however, a $256.8 trillion tectonic shift in global financial assets might explain the stock market’s abnormal stubbornness as no longer driven by unwavering optimism.

The Financial Stability Board recently reported that 51% of global financial assets are held by nonbank financial intermediaries (NBFI). These holdings in NBFIs grew at double the pace of those held in banks. Entities such as insurance, pensions, investment funds, trusts, even Starbucks or PayPal accounts, collectively hold more than half of the world’s wealth. Relative to the US, $94.5 trillion are held by these entities, making up 64.8% of total US financial assets. The impact of this shift is less of a change in ownership but rather a complete alteration of the engine.

To understand the scope of this transition lies in the idea of the great weighing machine, coined by the Father of Value, Benjamin Graham. This theory forms the foundation of stock market strategies where the price reflects a company’s fundamental value. However, in June 2021, Harvard professor Xavier Gabaix and University of Chicago Professor Ralph S.J. Koijen released their research on the inelastic market hypothesis (IMH), a theory that contradicted traditional thinking. In essence, the paper describes current market demand as inelastic, driven less by traditional pricing or valuation methods, but more by fund mandates and index distributions. To put it another way, market price movements could be explained through incentives and requirements rather than the balance sheet components produced by the companies themselves.

These entities are run with different models that invest indiscriminately. Insurance companies might sell their equities after a hurricane, driving prices down. Pension funds buy because their mandates require them, suddenly pushing prices up. Investors are prompted to rebalance their portfolio because of an asset price shock. Institutional investors recommend “toss it and leave it” approaches via passive investing vehicles. Koijen describes it succinctly: “What we’re suggesting is that a large fraction of the market is restricted by mandates, therefore not necessarily reacting to new information.”

Gabaix and Koijen go on to argue that equity prices reflect the cash inflows and outflows of the market as opposed to intrinsic value. As a result, the capital markets create a multiplier effect where $1 invested pushes market prices to $5. This contradicts traditional theories that market prices are not influenced by a singular dollar invested, but rather influenced by information on the economy or the assets themselves. If the inelastic market hypothesis is proven to be true, it would have massive implications that involve concentrations in indices, frequent mispricings, disconnection from the current economy, and aggressive volatility. All of which are common symptoms of today’s market.

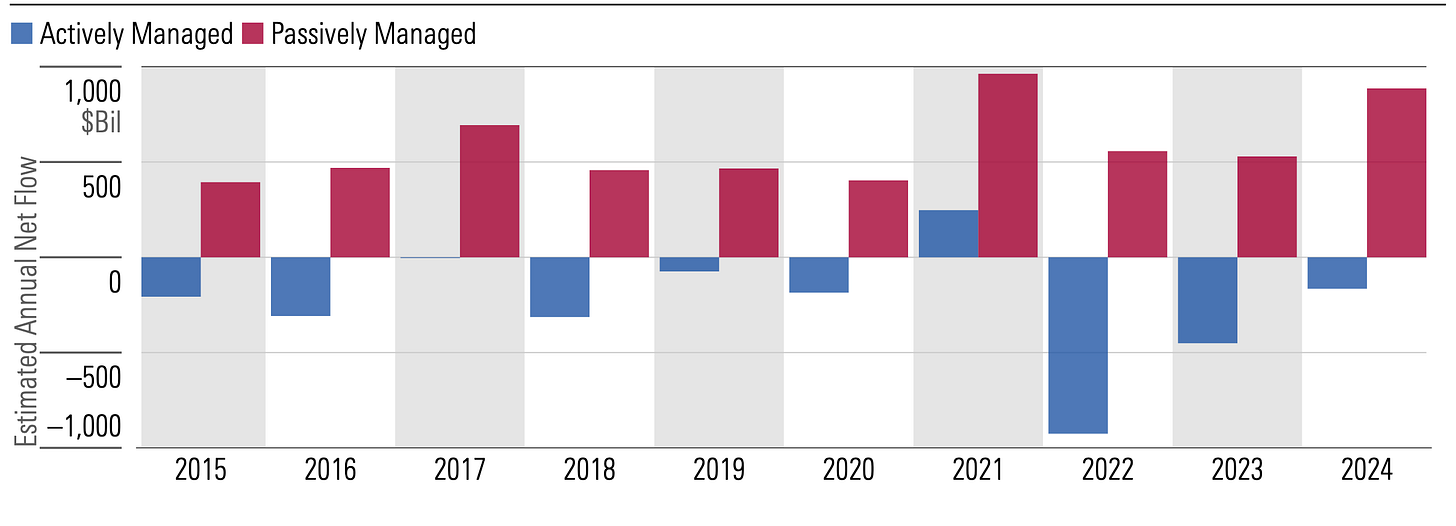

Throughout the paper, Gabaix and Koijen continuously use the phrase, “If true,” to emphasize the paper as an argument rather than a fact. However, in 2025, Morningstar reported that passive fund flows overtook active fund flows and have continued to dominate market share throughout the year. This, combined with newfound knowledge of the rise of NBFI held assets, the inelastic market hypothesis is slowly coming to fruition. As slow-moving and uninformed investors flood the market, investors that depended on traditional methods lose market share and may find it more difficult to understand and influence the markets.

This new environment, where markets depend on the ebbs and flows of funds, is packaged with both unforeseen benefits and consequences. Investing may become more straightforward, especially as the masses are supported by more than just retail investors. In this regard, herd mentality snowballs in strength while opportunities for contrarian investing become increasingly scarce and risky.

However, straightforward does not necessarily mean smooth. “Shocks to flows and investor demand have an outsize effect on prices, leading to volatile markets,” says Koijen. Wealth disruptions such as mass unemployment, natural disasters, or asset fluctuations are among the different types of shocks that can create volatile markets and trigger other domino effects.

Other investing strategies may become less viable. For example, small caps with strong fundamentals may not build the same momentum as in the past, whereas large caps will continue to face overvaluation. This is seen in today’s markets as indices such as the Russel 2000 have struggled to outperform the S&P 500 in recent years.

However, the most chilling consequence is uncertainty. As old methods are tossed aside, consequences aren’t just detrimental but also blindsiding. For now, market prices are still driven by a combination of intrinsic valuation and fund flows, but the tides are certainly changing. Amid the unsettling future of today’s markets, Gabaix and Koijen conclude on an optimistic note, as there are “A rich number of questions that hopefully economists will be able to answer in the coming years.”

Thanks for reading! Article by Calvin Huang, read the original here on Substack.